After just over a year, Contrarian Miner is nearing the end of its short life. For all the right reasons – I am taking the money out of the portfolio to put into a mining fund that I am starting in JV with a US group. I hesitate to use the words “hedge fund”with all that that implies, so lets call it a private fund that can go both long and short. Aiming to start trading with our own money in January followed by a “friends and family” funding round in late Q1 17.

That means I have about 6 weeks to turn the whole of the Contrarian portfolio into cash. And that poses something of a dilemma – in theory I want to be out of the market for as short a time as possible before I re-invest within the fund structure. So I should sell out on day x-1. But if the mining sector has a major pullback just as I need to cash…Already I have watched the value of the portfolio fall from a high of £174k to today’s value of £168,932.

So what I’m planning to do is to sell down selectively, anything I think might be at short term highs or particularly exposed to a pullback on a 2 month view. And leave the rest to the last minute.

So far I have sold…

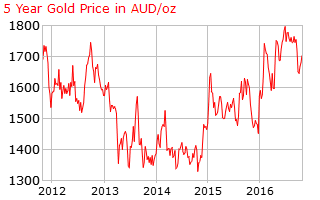

- 1/2 my holding in PHPD (Palladium ETF) last last week at $70.00 and the remainder today at $73.52. At $771/oz the Palladium price is at its highest level since June 15 and up 43% in the last year against both gold and platinum down 11%. See chart below.

- Half my holding in Tullow (1300 shares at 279p – a 23% gain). The shares are up more than 5% today ahead of an OPEC decision that could still go either way. Contrarian Portfolio was 15% oil before this sale.

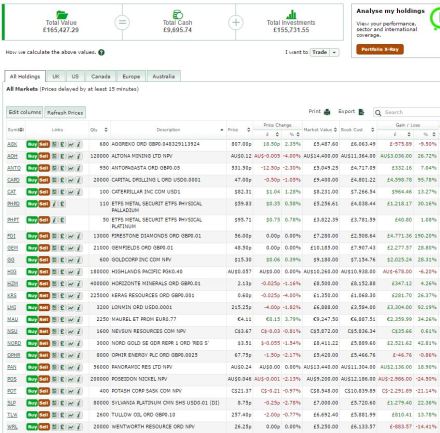

Portfolio stands at £169,391 today with £22,406 in cash. See below.