Farewell from Contrarian Miner

In my last Contrarian Miner post at the end of November, I said I would be selling down the portfolio over the next 6 weeks. For various reasons involving the complexities of Delaware LLC’s and offshore feeders that I will not bore you with, it’s taking a touch longer than that. But the process has begun and I thought in the interests of completeness I would officially bid you all farewell with a last look at Contrarian Miner.

It’s been quite a challenging final period for Contrarian Miner. Until very recently, the precious metals and particularly 15% platinum exposure has looked a bit premature as has the 12% exposure to junior nickel companies. Relative to a FTSE 350 benchmark which is comprised 86% of Rio Tinto, BHP Billiton, Anglo American and Glencore, the result has been that the index has almost caught up with me from behind. See chart below.

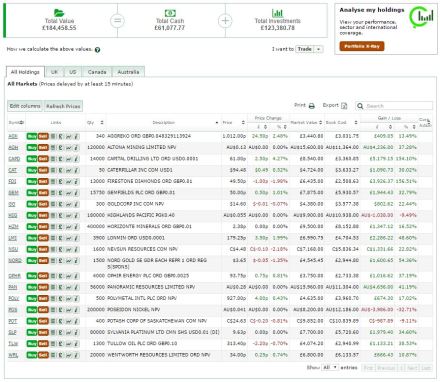

However in absolute terms the portfolio is ending on a high note, and one of which I am very proud. The Contrarian Portfolio stands at £184,459 – up 84.5% since I started in November 2015. I currently have £61,077 in cash (mostly dollars)- roughly a third of the portfolio – which seems a sensible point to call an end to tracking the performance of the Contrarian portfolio performance (and by extension my very short blogging career).

Farewell followers. Final portfolio snapshot below…

The beginning of the end for Contrarian

After just over a year, Contrarian Miner is nearing the end of its short life. For all the right reasons – I am taking the money out of the portfolio to put into a mining fund that I am starting in JV with a US group. I hesitate to use the words “hedge fund”with all that that implies, so lets call it a private fund that can go both long and short. Aiming to start trading with our own money in January followed by a “friends and family” funding round in late Q1 17.

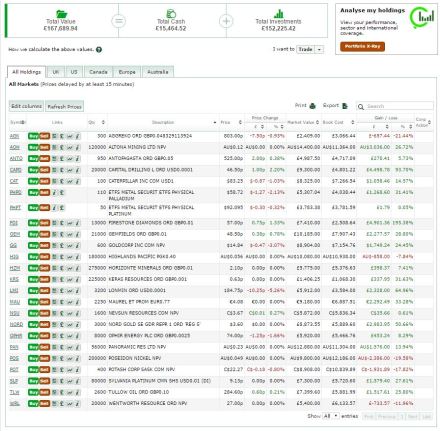

That means I have about 6 weeks to turn the whole of the Contrarian portfolio into cash. And that poses something of a dilemma – in theory I want to be out of the market for as short a time as possible before I re-invest within the fund structure. So I should sell out on day x-1. But if the mining sector has a major pullback just as I need to cash…Already I have watched the value of the portfolio fall from a high of £174k to today’s value of £168,932.

So what I’m planning to do is to sell down selectively, anything I think might be at short term highs or particularly exposed to a pullback on a 2 month view. And leave the rest to the last minute.

So far I have sold…

- 1/2 my holding in PHPD (Palladium ETF) last last week at $70.00 and the remainder today at $73.52. At $771/oz the Palladium price is at its highest level since June 15 and up 43% in the last year against both gold and platinum down 11%. See chart below.

- Half my holding in Tullow (1300 shares at 279p – a 23% gain). The shares are up more than 5% today ahead of an OPEC decision that could still go either way. Contrarian Portfolio was 15% oil before this sale.

Portfolio stands at £169,391 today with £22,406 in cash. See below.

Taking profits on ANTO

Taking profits today on Antofagasta – sold all 950 shares I held at 679p today. The stock is up 39% since I bought it last November. Sure, it could go a lot further long term but I am looking to increase the cash balance in Contrarian and this seems a sensible place to start. Copper has had a good run recently and I think will likely pause for breath, and ANTO likewise. The value of the Contrarian Portfolio stands at £171,512 with £12,519 in cash.

Buying more platinum (PHPT)

With platinum at a 6 month low of US$930/oz, earlier this week I topped up my holding in the ETFS Physical Platinum ETF (PHPT). The fund holds the physical metal with each unit of the fund back by just under 1/10th of an ounce . I bought a further 50 shares at $88.51.

The logic is unchanged since I first bought into this ETF – there is lots of more complicated analysis behind my thinking, but in very simple terms the 5yr high for platinum was at US$1,734/oz and the 5 year low at $816/oz. A very unequal risk reward relationship

At current prices, producers have to cut supply further or at the very least not invest in new capacity or they simply can’t survive (as good reason to be buying the ETF and a bit cautious on the producers still).

Following this purchase, I now hold 15% of the Contrarian Portfolio in PGMs.

One year down and 65% up

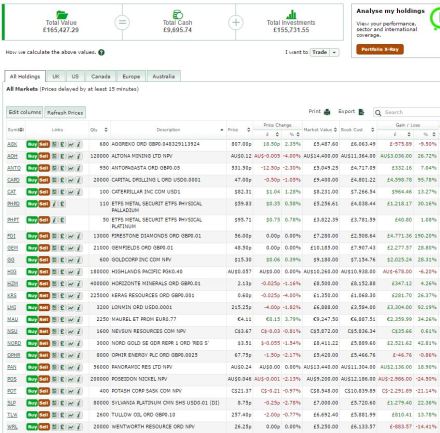

I can hardly believe it’s been a year since I started Contrarian Miner. But it has – on 5th November 2015 I had £100,000 in cash waiting to be spent. A year later the value has grown to £165,427 – well on my way to achieving my stated objective of doubling my money within 2 years.

Hitting the one year mark, I thought I would take a moment to reflect on the performance of the portfolio and some of the good/bad decisions I have made along the way.

The portfolio is up 65% over the past year, against the FTSE 350 Mining (Total Return) Index up 48% over the same time period, so I am very pleased. Nevertheless, I can’t help feeling a little disappointed with the portfolio’s more recent performance as it has lagged on a relative basis in recent months. See chart below.

Of the £65,427 gain:

- £25,460 is unrealised capital gains:

- Includes significant unrealised gains on Capital Drilling (£4,600), Firestone Diamonds (£4,771), Lonmin (£3,304) and Gemfields (£2,278)

- c£38,460 is realised capital gains

- Of which 50% was from 6 stocks – Roxgold £5,025, Fresnillo £4,450, Semafo £4,320, Firestone Diamonds £4,795 – in addition to the unrealised gain above, Amara Mining £2,960 (I sold on the bid) and Centamin Egypt £1,981

- Don’t even ask about Capital Gains Tax

- c£1,500 is from dividends – a modest 1.5% dividend yield on the portfolio this year

Looking back what would I have done differently if I started all over again?

The funny thing is that I already knew my investment weakness – buying too early and selling too early. And despite knowing that and trying to sit on my hands, I sold almost everything I realised profits on way too early and put the money into other stocks which I still have great confidence in, but most of which have yet to move. Meanwhile my top performing stocks continued their strong runs.

Had I invested in the same starting portfolio last November but then done nothing for the rest of the year I suspect I would have been up far more – I haven’t actually mathematically back tested this so I am extrapolating from a selection of stocks I have looked at, but I’m pretty sure I’m right. Probably better not to actually test that – it suggests I have wasted a great deal of time between last December and today. So my new year’s resolutions are to:

- Trade less,

- Don’t underestimate how far stocks can move – just because something is up 100% does not mean it does not have a lot further to run,

- Before rotating from top to bottom performing sub-sectors (e.g. from gold to nickel) wait, and then wait some more, and then wait some more. Let momentum work for me, just a tiny little bit (don’t worry I am still a Contrarian).

Portfolio below (at Friday’s closing prices).

Why I’m not buying Horizon Gold IPO

Shareholders in Panoramic Resources (ASX: PAN) have been offered priority in the upcoming Horizon Gold IPO (the spinout of the Gum Creek gold project from PAN). I bought PAN for the nickel assets, ascribing no value to either the gold or PGMs. But ever one for a bargain, I’ve been doing some homework on Gum Creek but decided against.

Horizon will have a post IPO market cap (at the A$0.40/share offer price) of A$30.6m of which A$13.65m will be the new cash leaving an A$16.9m EV. With a gold resource of A$1.25Moz that is an EV of just A$14/oz- arguably a bargain, right? But:

- The development studies will build on the March 2016 scoping study for free milling gold. That estimated AISC as A$1,209/oz (US$931/oz at current exchange rates but lets not forget the A$ was a parity not that long ago),

- The scoping study saw production of just 290koz over a 6 yr life (i.e. even assuming a gold price of A$1,700/oz, not that much of the 1.25Moz “resource” is economic)

- Even at a gold price of A$1,700/oz the mine generated EBITDA of just A$29m a year and thus takes more than 2 yrs of its 6yr life to pay back its A$62m capex

- They will be spending the A$13.5m raised in the IPO over the next 2 years on exploration and development studies – this is quite a “slow burn” opportunity

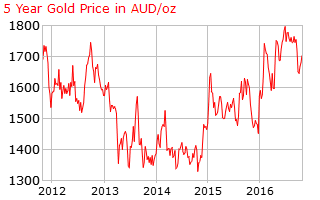

And here is what the gold price in A$ looks like over the last 5 years. A$1,700/oz is close to 5yr highs. Sure the USD gold price may move higher, but currency may move in the opposite direction. For me this is not a value opportunity. Now perhaps there is lots of exploration potential and room to optimise. But I don’t see clear value so Horizon Gold is not for me.

As a PAN shareholder I am, however hoping other feel differently and it flies. They keep 51% of Horizon so at the IPO price that is worth A$15m. PAN also has A$19m in cash leaving an EV for the nickel assets (and PGMs) of just A$66m.

Buying more AGK and HZM

In my last post I mentioned that I am going to be reviewing some of the laggards in the portfolio is to see whether I should be considering cutting losses.

Instead today I have bought a further 380 Aggrekko at 781p. The stock is down 23% since I bought a small stake on 13 September which is not terribly cheering. But reviewing the performance and prospects for the company I see no reason for a change of heart. Over the past 5 years Aggreko has generated average annual EBITDA of US$584m or just 5.2x the current enterprise value.And whilst net debt has risen this year, it is <1.3x EBITDA with plenty of funding headroom in place. There is lots of talk about increased competition in the sector. And perhaps that may indeed erode short term margins, but on the other hand Aggreko has a very strong presence in North America where the prospects for a pickup in oil and gas activity are good – and I am not convinced Karadeniz Energy is likely to find it easy to compete in that market. For me this offers at least the 50% upside potential I am looking for in the Contrarian portfolio. And it certainly ticks the Contrarian box. Analysts seem to hate this stock.

On another note, I have also topped up my holding in micro-cap Horizonte Minerals, buying another 125,000 shares at 2.2p. The share are up just 10% since I bought them in July against the FTSE 350 mining index up more than 20% over the same period so they count as underperformers. But the 3 Oct results from the revised PFS on Araguaia incorporating the Glencore resource are phenomenal. Capex is down to US$354m (from $582m) and cash costs are down to $3.15/lb from $4.16/lb but production is virtually unchanged at 14.5ktpa (prev 15ktpa). That means that the nickel price needed for this project to really work is c$13,000/t down from c$18,000/t previously and able to compete head-on with Indonesian NPI. The placing announced today to fund feasibility study work also buys them plenty of time, so the clock is not ticking for this company even if the nickel market stays tough. Even at a very conservative long term nickel price of US$12,000/t the project has an NPV of US$328m compared to post-placing market cap of $31m. Convincing enough?

The value of Contrarian stands today at £168,571 with £9,689 in cash.

Reducing Tullow (TLW)

Sold 900 Tullow at 284p reducing my holding to £7,400 or 4.4% of portfolio. The stock is up 26% since I bought it and usually I would be looking for more but oil stocks had crept up to 19% of Contrarian’s holdings (Maurel et Prom, Ophir, Tullow and Wentworth) an this is supposed to be a mining fund! So with Tullow up 31% in the last month it seemed a sensible point to trim.

The value of Contrarian stands at £167,690 – it has not been keeping pace with the index in the last month which is frustrating. I may need to do a cleanup and work out whether all the underperformers really are stars waiting to shine (or just dogs). Could do with a few realised tax losses while I’m at it.

Portfolio below. Rather long cash, not entirely by accident.

FDI produces first diamonds but no-one cares

So much for that gut feel I had about something being not quite right at Firestone – they announced this morning that they have produced their first diamonds including a fancy yellow with recoveries as expected.

And the price is, hang on, unchanged? In fact they are 54.5p bid which is marginally below the 55p I sold them for before this momentous news. How odd.

Fear vs Greed

Sold another 4,500 Firestone Diamonds (FDI) at 55p leaving me still holding 13,000 shares.

The shares are up 185% since I bought them but arguably could still double from here based on the potential value of the mine once in production.

However (as I noted on the day) the company’s rather vague announcement on 6th October did little to reassure me that all is 100% on track with the commissioning. They promised a further update week beginning 17th October. Perhaps I was wrong to expect the announcement early in the week but I did so I keep wondering where it is. The fact is, having promised it they will have to put something out tomorrow good or bad, and right now I can’t shake the worry it’s the latter. I have no rational evidence – just a funny feeling that something in the tone of the last announcement wasn’t quite right. In any event I’ve made good money on this stock and I still hold plenty, but I am letting fear rule over greed for now.

Will probably regret it tomorrow.