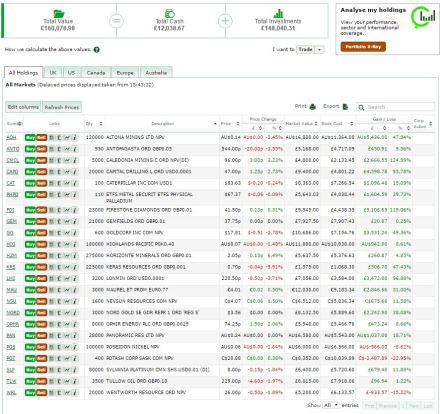

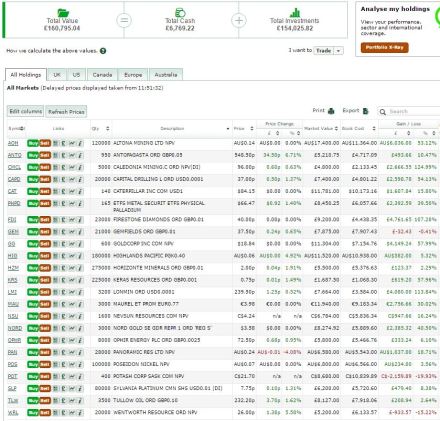

I really like the prospects for nickel- the price hit US$10,755/t yesterday, its highest level in nearly a year as the Philippine government continued to up the rhetoric in its crackdown on mining companies. But the price is still well below the marginal cost of around US$13,000/t and it seems to me that gap could close rapidly.

For me the best way to capitalise on the upside for nickel is through juniors, but I am well aware of the risks associated with investment in a single junior mining company – not least that management goes off on a tangent (see Keras Resources, down 40% in a week since the company admitted its small scale gold strategy is not – yet – working).

So I have chosen a set of three juniors to play the nickel theme:

- Panoramic Resources (ASX: PAN). I was already a holder of this stock but last week bought another 15,000 shares at A$0.21/share. Previously a producer, the company mothballed its mines in response to low prices. They can quickly be brought back on line with potential production of 20ktpa at cash costs of US$10-12,ooo/t it needs a nickel price of slightly more than US$13,ooo/t to start to come back on stream. The company has an enterprise value of US$63m of which theoretically cUS$11m is Gum Creek gold soon to spin off through IPO.

- Poseidon Nickel (ASX:POS). A new holding for me I bought 100,000 shares today at A$0.065. Like Panoramic, Poseidon holds mothballed mines which have produced recently and can readily be brought back to life – in Poseidon’s case assets bought from Norilsk. Again operating costs are $10-12,000 and it needs a price of $12,000-13,000/t for these assets to think about restart. We are not far off that already. The lithium potential may add to the story depending on your view (personally I am a contrarian and hence Lithium is not high on my wish list right now, but there it is).

- Horizonte Minerals (London: HZM). Hoping to add to the 100,000 shares I already own. This is rather a different beast to the two Aussies – a greenfield project in Brazil that will need a higher nickel price to justify investment. But world class in scale and I think a fantastic opportunity for the long term. I like management who have stuck to the strategy despite tough times.

Elsewehere in the Contrarian Portfolio, Maurel et Prom is up 36% today to €3.85 after the Chairman and CEO, Henin, agreed to sell his 24.5% stake in the company to Indonesian State firm Pertimina at €4.20/share with a kicker to €4.70/share if the oil price exceeds $65/barrel for more than 90 consecutive days in 2017. Shares still trading as a significant discount to the offer price and to what I think is their value so I will continue to hold.

Contrarian stands at £153,134. Portfolio below.