Late last week, I made a few changes to the portfolio continuing to reduce gold exposure and introducing some fresh ideas.

- I sold the remainder of my Roxgold (3500 at C$1.40) – at a 115% profit. As a reminder, this is what I said when I sold the first lot at 113p on 13 April:

“At the current gold price the company would generate around US$50m in cash each year, which makes for a seemingly generous FCF yield of 13% based on the current EV of just over US$380m. However, the reserve life of the mine is c8yrs, so at the current gold price the mine would generate cUS$400m in undiscounted free cash flow over the life of mine compared to an EV of US$380m.Sure the gold price could rise or additional resources could be converted to reserves. But given that its a pre-production asset in Burkina Faso, I’d say its pretty fairly priced right now and am taking some profit. Haven’t decided what to do with the other half – I have a nasty habit of selling things too early so I am tempted to hang on for a bit and see what happens”

That rationale is unchanged – except for the gold price up 3% and the share price up 24% – so I am now exiting this holding.

- Sold half of my Semafo shares – 900 at C$5.98 – a 92% profit. No particular reason not to like Semafo but feel there is better upside elsewhere. Keeping half.

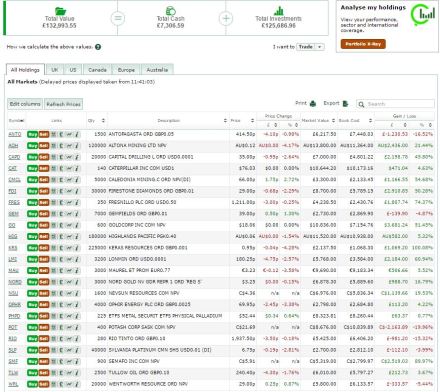

- Bought 40,000 Sylvania Platinum (London: SLP) at 7p. Sylvania has a decent management team and is one of the only South African platinum plays without significant labour issues as it is dump retreatment. EV just $20m and yet profitable and cash flow generative. Looks like an EV/EBITDA of <2x before you even take into account the rising platinum price. Production starts to decline from 2018, but by then I’ll be long gone.

- Bought 7,000 Gemfield (London: GEM) at 40p. I have long liked the Gemfields story – coloured gemstones with marketing as important as the mining – but it has been difficult to argue that it’s cheap. Arguably that may still be the case, but at 40p it’s certainly easier to make the case than it was at 68p. Unusually for me this is not a “value stock” but I like the idea, I like the management and the company generates cash as well as genuine and growing profits.

The value of Contrarian stands at 132,994. For some reason I am feeling despondent about Contrarian which has been trading sideways for months. But I am up 33% since inception and have outperformed the FTSE350 Mining index by 36% , so I have no real reason to be glum. Portfolio below